Is Your Bank on the Problem Bank List?

The Federal Deposit Insurance Corporation, the federal agency in charge of safeguarding the nation’s bank deposits, maintains a Problem Bank List. This list contains the names of institutions that are likely to have weak capital positions that can lead to failure.

The Federal Deposit Insurance Corporation, the federal agency in charge of safeguarding the nation’s bank deposits, maintains a Problem Bank List. This list contains the names of institutions that are likely to have weak capital positions that can lead to failure.

The FDIC does not publicize the list for fear of causing a run on the banks involved. An unofficial Problem Bank List is published by calculatedriskblog.com and contains the names of institutions that have been issued enforcement actions by banking regulators. The unofficial Problem Bank List currently totals 148 institutions compared to a total of 123 on the official FDIC confidential Problem Bank List.

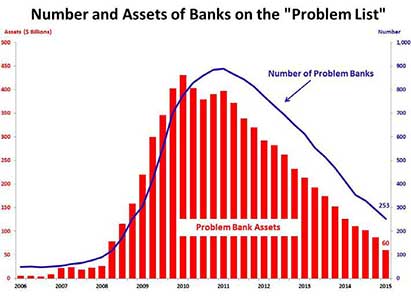

The number of banks on the FDIC Problem Bank List totaled 123 problem banks at December 31, 2016, down from 183 at December 31, 2015. The number of Problem Banks has declined by 86% from 884 at December 31, 2010.

The historic low for the Problem Bank List was reached in the third quarter of 2006 with 47 banks. The number of banks on the FDIC’s Problem Bank List remains at historic highs. In the decade prior to the banking crisis that began in 2008, the average number of problem banks was less than 100. Problem Banks now account for 2 percent of all FDIC insured banking institutions. As of December 31, 2016 there were 5,913 FDIC insured banking institutions with FDIC insured deposits of $6.92 trillion. The FDIC Deposit Insurance Fund (DIF), which protects insured depositors from loss when a bank fails, had a balance of only $83.2 billion at December 31, 2016 for a reserve ratio of 1.20%. Current law requires the FDIC to rebuild the DIF to to a minimum reserve ratio of 1.35% by 2020.

Total assets held by troubled institutions at December 31, 2016 amounted to $27.6 billion, an increase of $2.7 billion from $24.9 billion in the previous quarter.

In general, banks included on the Problem Bank List have serious deficiencies with their finances, operations, or management that threaten their continued solvency. Once a bank is included on the list, they are subject to closer regulatory scrutiny. They can also expect to receive instructions from regulators about what steps must be taken to rebuild their financial strength. The FDIC list of Problem Banks is comprised of banks with a CAMELS rating of 4 or 5. CAMELS stands for Capital Adequacy, Asset quality, Management, Earnings, Liquidity and Sensitivity to market risk. The CAMELS rating scale is from 1 to 5, with 5 being the weakest and 1 being the strongest.

The pace of bank failures increased dramatically from 25 bank failures during 2008 to 157 during 2010. The number of bank failures has been declining since the peak year of 2010 but a total of 513 banks have failed since 2008. The number of banking failures has now declined every year since 2010.

For all of 2013 there were a total of 24 banking failures, compared to 51 during 2012. During 2014 a total of 18 banks failed.

Banking Failures Since 2008

Year Number of Bank Failures

2008 25

2009 140

2010 157

2011 92

2012 51

2013 24

2014 18

2015 8

2016 5

2017 5

Total 525

During 2014 a total of 18 banks failed with total assets of $3.1 billion in assets and losses of $398.8 million for the FDIC Deposit Insurance Fund. A total of 24 banks failed during 2013 with total assets of $6.1 billion and losses to the FDIC of $1.17 billion. During 2012, a total of 51 banks with total assets of $12.0 billion failed, costing the FDIC Deposit Insurance Fund $2.51 billion in losses. A total of 92 banks failed during 2011, resulting in losses to the FDIC Deposit Insurance Fund of $7.22 billion. During 2010, a total of 157 banks failed, the most since 1992 when 181 were closed. Banking failures during 2010 cost the FDIC Deposit Insurance Fund $26 billion, bringing the fund balance to below zero. A total of 140 institutions failed during 2009 compared to only 25 during 2008. There were only 3 bank failures during all of 2007. No banks failed during 2005 and 2006.

For the week ending May 5, 2017, there was one bank failures. A total of 5 banks have failed so far during 2017. The cost to the FDIC Deposit Insurance Fund for the 2017 banking failures currently totals $6.3 billion. The 5 failed banks had total assets of $6.3 billion.

The number of problem banks remains extremely elevated five years after the banking crisis started in 2008. At the end of 2007, there were only 76 banks on the Problem Bank List compared to 123 as of December 31, 2016. This is a very troubling number of problem banks, considering the amount of aid that was given to the banking industry by the government and the fact that the economy has stabilized since the depths of the banking crisis.

Typically, the number of troubled banks would decline rapidly after a recession as economic conditions improve and insolvent banks are closed by regulators. The chart below shows the quarterly change in problem banks due to bank failures and the net change in banks classified as “problem banks”.

Why Are Problem Banks Allowed To Stay Open?

The reason regulators do not close more insolvent banks may be due to the fact that the FDIC Deposit Insurance Fund (DIF) had a balance of only $83.2 billion at December 31, 2016. A number of large banking failure could deplete the entire insurance fund and cause panic among bank depositors. The DIF reserve ratio at March 31, 2015 was 1.20% percent, far below historical ratios. The FDIC is currently backing every $1 million dollar of deposits with only $12,000 of reserves. The FDIC currently provides deposit insurance on $6.9 trillion. By law the FDIC is required to increase the reserve ratio to a safer level of 1.35% by 2020.

Total deposits insured by the FDIC Deposit Insurance Fund have increased dramatically from $3.62 trillion in 2004 to $6.9 trillion at December 31, 2016. Total assets of all FDIC insured institutions at December 31, 2016 were $16.78 trillion.

The FDIC has already publicly acknowledged that the DIF must not be allowed to fall to dangerously low levels when it approved a measure that required insured institutions to prepay 3 years of FDIC insurance premiums of about $46 billion at the end of 2009.

The FDIC believes that it is important that the fund not decline to a level that could undermine public confidence in federal deposit insurance. A fund balance and reserve ratio that are near zero or negative could create public confusion about the FDIC’s ability to move quickly to resolve problem institutions and protect insured depositors.

Even though the FDIC has significant authority to borrow from the Treasury to cover losses, a fund balance and reserve ratio that are near zero or negative could create public confusion about the FDIC’s ability to move quickly to resolve problem institutions and protect insured depositors. The FDIC views the Treasury line of credit as available to cover unforeseen losses, not as a source of financing projected losses. The FDIC projects that the reserve ratio will fall to close to zero or become negative in 2009 unless the FDIC receives more revenue than regular quarterly assessments will produce, given the rates adopted in the final rule on assessments.

FDIC Requests Massive Line Of Credit From The Treasury

During the beginning of the financial crisis the FDIC projected a substantially higher bank failure rate over the next couple of years and admitted that the DIF could be completely wiped out which is exactly what happened in 2009. The FDIC DIF fund of $83.2 billion at December 31, 2016 provides deposit insurance protection on $6.9 trillion of insured deposits – see DIF Fund Running on Empty.

The FDIC views the line of credit at the Treasury as being available to cover “unforeseen losses”. If that is the case, then the FDIC must have seen the potential for massive “unforeseen losses” since it requested and was approved for an increase in the line of credit from the Treasury to $500 billion from the current $30 billion. This increased line of credit would be available to address “systemic risks” and potentially allow the FDIC to inject funds into banks that otherwise would face closure. The FDIC has admitted that it cannot presently resolve more failed banks without depleting its insurance fund and potentially panicking the public.

On May 20, 2009 the President signed into law a bill authorizing increased FDIC insurance coverage on deposits as well as an increase of the FDIC’s line of credit with the Treasury.

The new law increases the FDIC’s line of credit at the Treasury to $100 billion from $30 billion. The FDIC’s viewpoint on the line of credit with the Treasury was recently spelled out by the FDIC as follows:

Even though the FDIC has significant authority to borrow from the Treasury to cover losses, a fund balance and reserve ratio that are near zero or negative could create public confusion about the FDIC’s ability to move quickly to resolve problem institutions and protect insured depositors. The FDIC views the Treasury line of credit as available to cover unforeseen losses, not as a source of financing projected losses.

Should extraordinary circumstances arise, the FDIC also has the authority to borrow up to $500 billion from the Treasury with the consent of both the Federal Reserve and the Treasury Department.

One “Special Assessment” Was Not Enough

The FDIC imposed a special assessment in the amount of 5 basis points on each FDIC depository institution’s assets as of June 30, 2009. This special mid year assessment proved inadequate due to numerous banking failures and in late September 2009, the Deposit Insurance Fund (DIF) was depleted by the increasing number of banking failures. The FDIC took additional steps to increase the DIF by requiring FDIC insured financial institutions to prepay three years of deposit assessments. This measure added $46 billion to the DIF. The FDIC took this action in recognition of the reality that hundreds of additional banks could fail (see FDIC To Bolster DIF With Prepaid Assessments). Since 2008, a total of 525 banking institutions have failed.